Weekly Market Commentary – 1/19/2024

January 19, 2024

Fed makes another move – is it the last?

US Markets gained ground in the second week of 2024, attributed to mega-cap issues in the Information Technology and Communication Services sectors. The Equal-weight S&P 500 was up 0.2%, while the Mega-Cap index was up 3.9%. Notably, the S&P 500 touched its all-time high before giving some of those gains back on what was perceived to be a lackluster start to Q4 earnings. JP Morgan, Citibank, Wells Fargo, and Bank of America kicked the earnings season off, but the results were blah, and the outlook was cautious. Semiconductor company Microchip’s outlook was dim, as was the outlook of Delta Airlines, and both companies fell after their earnings announcements. Boeing endured a tough week as the company’s CEO acknowledged that the company was in error for loose bolts related to last weekend's Alaska Air incident. The stock fell nearly 13% on the week.

Fed rhetoric was decidedly hawkish this week as Fed Presidents Williams and Mester pushed back on the notion that the Fed will be cutting rates at their March meeting. The Economic calendar was centered on inflation data that came in with mixed results. Interestingly, the probability of a March rate cut increased to just under 80% from 68% in the prior week. Of note, the SEC approved several Spot Bitcoin ETFs that were up and trading the day after the announcement. Bitcoin and many of its proxies sold off after the announcement, suggesting some of this action was already priced in.

The S&P 500 gained 1.8%, the Dow added 0.3%, the NASDAQ outperformed by tacking on 3.1%, and the Russell 2000 was unchanged for the week. US Treasuries rallied across much of the yield curve, with shorter-tenured paper outperforming longer-duration paper. The 2-year yield fell twenty-four basis points to 4.15%, while the 10-year yield fell by nine basis points to 3.95%. Oil prices declined, but the sell-off was smaller than one might have expected, given the announcement that the Saudis were cutting prices and considering increasing production. The news may have been less impactful, given increased tensions in the Red Sea where the US and UK, in a joint effort, targeted Houthi assets in Yemen. Gold prices were little changed at $2051.60 an Oz. Copper prices fell by $0.07 to 3.74 per Lb. The US Dollar index was steady at 102.41.

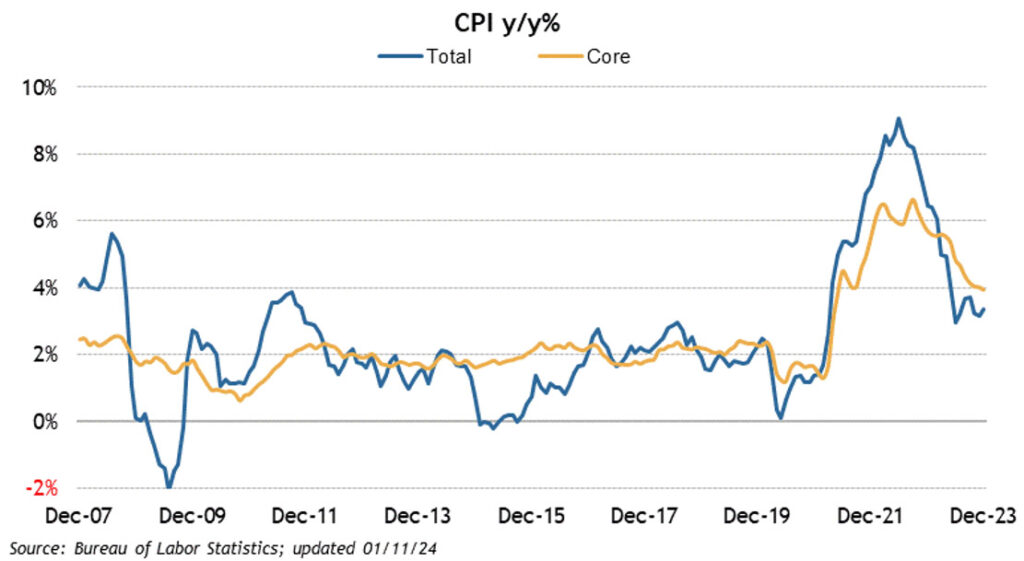

The Consumer Price Index (CPI) was slightly hotter than expected. The headline number was up 0.3% in December versus the street estimate of up 0.2%. On a year-over-year basis, the figure rose 3.4% in December from 3.1% in November. Core CPI, which excludes food and energy, also rose 0.3%, above the 0.2% consensus estimate. On an annual basis, the figure rose 3.9% in December, down from 4% in November. Shelter prices continued to rise and made up nearly half of the price gains. Wholesale prices showed much more improvement. The Producer Price Index (PPI) fell .01% in December versus the expectation of a 0.1% increase. Core PPI came in flat relative to the street’s expectation for a 0.2% gain. The labor market continued to shine. Initial claims came in at 202k, while continuing claims were down 34k to 1.834m.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involve risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.

{kind=link}

{kind=link}

Weekly Market Commentary – 12/30/24

Read more