Weekly Market Commentary 4/5/2024

April 5, 2024

Weekly Market Commentary 4/19/2024

April 19, 2024

Financial markets pulled back for the second consecutive week as investors continued to recalibrate monetary policy expectations and assess the most recent conditions in geopolitics.

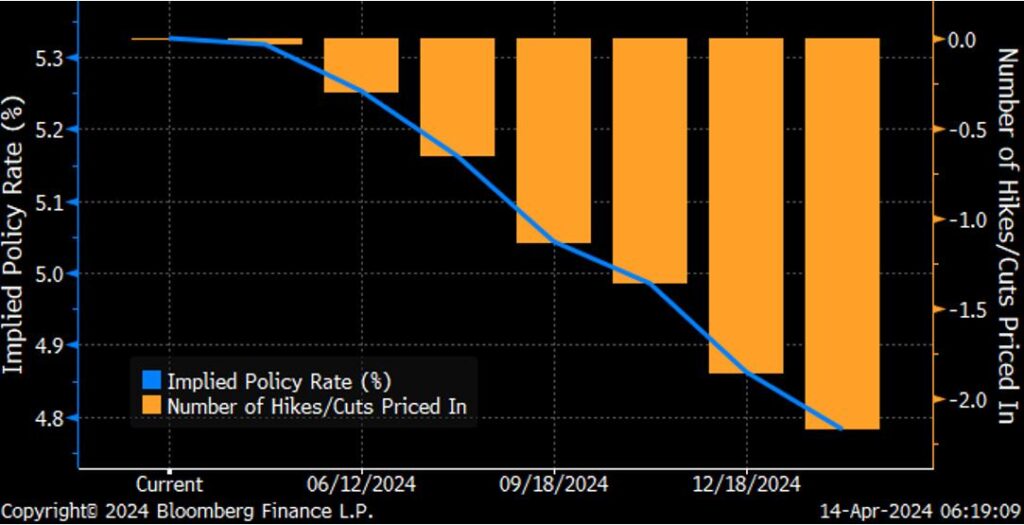

A stronger-than-anticipated Consumer Price Index, announced on Wednesday, pushed expectations for the timing of the first rate cut to September from June. The hotter print also modified expectations of how many cuts the market expects this year from three to two. The news significantly impacted US Treasuries across the curve and gave equity investors a reason to take money off the table. Rate-sensitive sectors such as Real Estate and Financials were particularly hard hit during the week.

The banks kicked off earnings season on Friday, and the results were disappointing. JP Morgan’s CEO, Jamie Diamond, echoed the cautious sentiment he provided in a shareholder letter sent early in the week on the earnings conference call while delivering an in-line expectation for the coming quarter. The stock fell 6.47% after their earnings announcement, catalyzing a broader sell-off within the Financial Sector.

There were numerous reports out Friday that there was an imminent attack planned on Israel by Iran. Traders fearful of an escalation of tensions in the region bid up safe-haven assets and sold risk assets. The reports come after Israel attacked Iran’s embassy in Syria, where 7 Iranian officials were killed. Hezbollah, an Iranian proxy in Lebanon, continues to launch attacks from the north, while the Yemen-based Houthis continue to be a menace for assets in the Red Sea. Reports suggest that Iran will hit Israel with drones and missiles in the next couple of days. As I write this recap, an Iranian paramilitary group has taken control of an Israeli-owned tanker in the Strait of Hormuz and directed it to Iranian waters. The Strait of Hormuz is considered a significant shipping route and will undoubtedly put a bid into the energy markets.

There were numerous reports out Friday that there was an imminent attack planned on Israel by Iran. Traders fearful of an escalation of tensions in the region bid up safe-haven assets and sold risk assets. The reports come after Israel attacked Iran’s embassy in Syria, where 7 Iranian officials were killed. Hezbollah, an Iranian proxy in Lebanon, continues to launch attacks from the north, while the Yemen-based Houthis continue to be a menace for assets in the Red Sea. Reports suggest that Iran will hit Israel with drones and missiles in the next couple of days. As I write this recap, an Iranian paramilitary group has taken control of an Israeli-owned tanker in the Strait of Hormuz and directed it to Iranian waters. The Strait of Hormuz is considered a significant shipping route and will undoubtedly put a bid into the energy markets.

The S&P 500 fell by 1.6%, the Dow lost 2.4%, the NASDAQ shed 0.5%, and the Russell 2000 gave back 2.9%. US Treasuries yield increased across the curve despite a safe-haven bid into Treasuries on Friday. The 2-year yield increased fifteen basis points to close at 4.88% after trading north of 5%. The 10-year yield increased by twelve basis points to 4.50%, the highest level of the year. Commodities finished the week mixed. West Texas Intermediate Crude prices fell by $1.22 or 1.4%. Gold traded above 2400 before settling up $29.20 for the week at $2374.50 an Oz. Copper prices increased by $.02 to $4.26 per Lb., the highest level in two years. The US dollar index screamed higher, gaining 1.7% on the week and closing at 106.2.

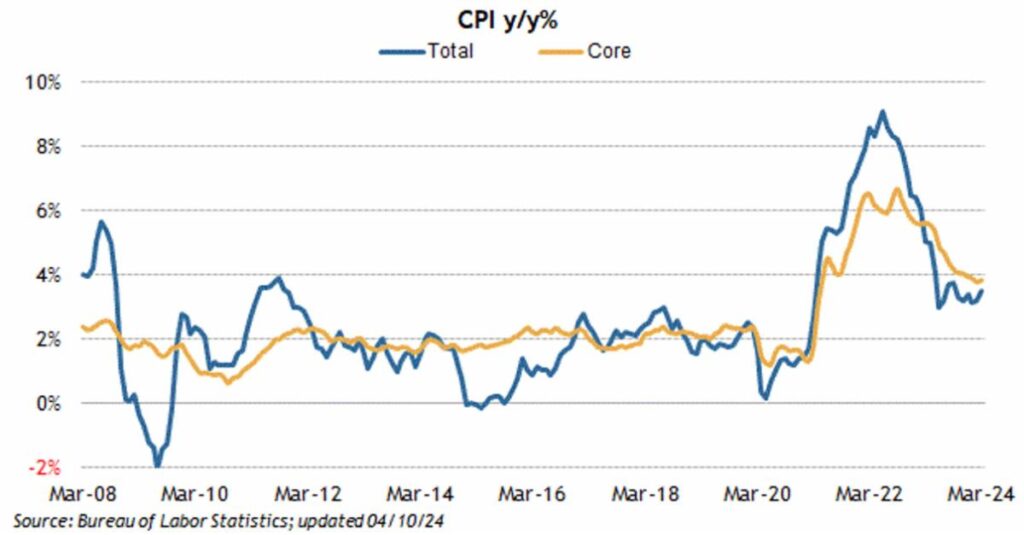

The economic calendar was centered on the Consumer Price Index, which showed higher-than-expected inflation on both the headline and core readings. Headline CPI increased by 0.4% versus an estimated 0.3% and increased by 3.5% year-over-year, above the 3.5% increase registered in February. Core CPI, which excludes food and energy, rose by 0.4% and was up 3.8% year-over-year for the second consecutive month. The Producer Price Index showed less-than-expected price increases on a month-over-month basis but saw the year-over-year figure increase to 2.1% from 1.6% in February. Initial Claims came in at 211k versus an estimated 216k, while Continuing Claims increased by 28k to 1817k. The second preliminary look at the University of Michigan’s Consumer Sentiment saw it regress to 77.9 from 79. Small business optimism also saw a pullback.

{kind=link}

{kind=link}

Weekly Market Commentary – 12/30/24

Read more