Weekly Market Commentary 4/12/2024

April 12, 2024

Weekly Market Commentary 4/26/2024

April 29, 2024

Financial markets took another step back last week as investors grappled with increased tensions in the Middle East and the recognition that interest rates are likely going to be higher for longer.

Iran fired back at Israel last weekend with a barrage of drones and missile attacks. The move had been widely telegraphed- Israel was prepared and effectively defended itself. The worry for most investors is that these back-and-forth attacks continue and escalate into a much larger conflict. Israel responded with its own counter later in the week but did not inflect very much damage on Iranian assets; this was seen as a move to try and de-escalate the situation.

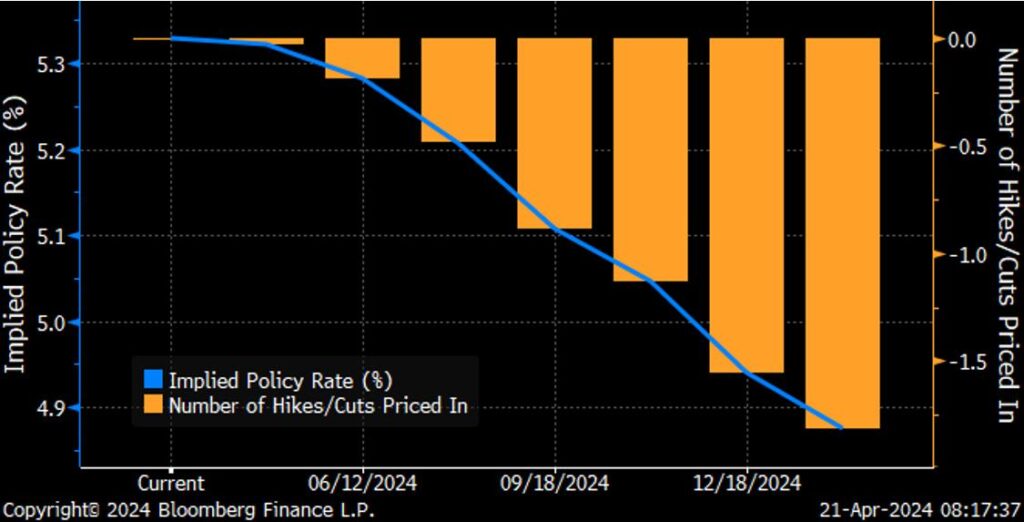

Last week, there were plenty of Federal Reserve officials to listen to for their latest reading on monetary policy. Fed Chairman Jerome Powell pushed the timeline out for when rate cuts would begin, referencing the hotter-than-anticipated inflation data over the last couple of months. Currently, there is a 65% possibility of a 25 basis point rate cut at the September meeting, and the market now expects 1 to 2 rate cuts this year. The higher-for-longer narrative has taken hold, with many market participants now thinking there may be no cuts this year. I think this idea of no cuts this year is what hit the market this week. We have been writing about the recalibration of rate cut expectations for some time, and we were wondering if the equity markets were ignoring what had been going on in the rates market- well the S&P 500 has now closed lower for six consecutive sessions.

The S&P 500 fell 3.1%, the Dow was unchanged on the week, the NASDAQ plunged 5.2%, and the Russell 2000 lost 2.8%. Mega-Cap tech was particularly hard hit as semiconductor stalwarts NVidia, ASML, and Taiwan Semiconductor were aggressively sold. The S&P 500 is off 5.6% from its recent all-time high. The US Treasury market continued to be under pressure and, interestingly, has not really provided any safe-haven qualities given the current geopolitical landscape. The 2-year yield increased by nine basis points to close at 4.97%, while the 10-year yield increased by twelve basis points to 4.62%. Of note, there was a decent 20-year US Treasury auction last week that came off the back of three not-so-good auctions in the prior week. Some risk premium came out of oil later in the week as tensions in the Middle East were softened. WTI closed down 4% to $82.09 a barrel. Gold prices increased by 1.6% or $40.30 to $2414.80 an Oz. Copper prices continued to soar, gaining 5% this week to close at $4.49 per Lb. Despite strong intervention from several emerging market central banks, the US dollar index closed the week with little change.

The S&P 500 fell 3.1%, the Dow was unchanged on the week, the NASDAQ plunged 5.2%, and the Russell 2000 lost 2.8%. Mega-Cap tech was particularly hard hit as semiconductor stalwarts NVidia, ASML, and Taiwan Semiconductor were aggressively sold. The S&P 500 is off 5.6% from its recent all-time high. The US Treasury market continued to be under pressure and, interestingly, has not really provided any safe-haven qualities given the current geopolitical landscape. The 2-year yield increased by nine basis points to close at 4.97%, while the 10-year yield increased by twelve basis points to 4.62%. Of note, there was a decent 20-year US Treasury auction last week that came off the back of three not-so-good auctions in the prior week. Some risk premium came out of oil later in the week as tensions in the Middle East were softened. WTI closed down 4% to $82.09 a barrel. Gold prices increased by 1.6% or $40.30 to $2414.80 an Oz. Copper prices continued to soar, gaining 5% this week to close at $4.49 per Lb. Despite strong intervention from several emerging market central banks, the US dollar index closed the week with little change.

The economic calendar was fairly quiet last week. Retail sales data showed that consumers are still out spending. The headline number came in at 0.7% versus an estimated 0.3%. The Ex-auto figure came in at 1.1% versus the consensus estimate of 0.6%. Housing data reported over the week was weaker than anticipated. Housing Starts, Permits, and Existing Home Sales missed the mark as 30-year Mortgage rates approach 7.5%. Initial Claims came in at 212k for the second week in a row, while Continuing Claims rose by 2k to 1812k.

The economic calendar was fairly quiet last week. Retail sales data showed that consumers are still out spending. The headline number came in at 0.7% versus an estimated 0.3%. The Ex-auto figure came in at 1.1% versus the consensus estimate of 0.6%. Housing data reported over the week was weaker than anticipated. Housing Starts, Permits, and Existing Home Sales missed the mark as 30-year Mortgage rates approach 7.5%. Initial Claims came in at 212k for the second week in a row, while Continuing Claims rose by 2k to 1812k.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involve risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted

{kind=link}

{kind=link}

Weekly Market Commentary – 12/30/24

Read more