Weekly Market Commentary – 1/26/2024

January 26, 2024

Weekly Market Commentary – 2/9/2024

February 9, 2024

It was a turbulent week on Wall Street as investors assessed the Federal Reserve’s decision on monetary policy while economic data and corporate earnings offered mixed results. Tensions in the Middle East escalated as the US hit Iranian proxy assets in multiple countries, even as reports suggest a cease-fire in Gaza was imminent.

The January FOMC statement came in pretty much as expected. There was no change to the policy rate, and a balanced tone on the path for rates that will be measured on the economic data received over the coming months. However, the feedback from Chairman Powell post statement was more hawkish than expected and catalyzed a sell-off in the equity and Treasury markets. The Chairman pushed back hard on the notion of a rate cut in March and insisted it was too soon to declare a victory on the inflation front. The probability of a rate cut in June fell to ~20% from nearly 50% at the end of last week on Powell’s push back and on a much stronger than expected Employment Situation Report. The probability of a May cut fell to 74% from 93.8% in the same time frame.

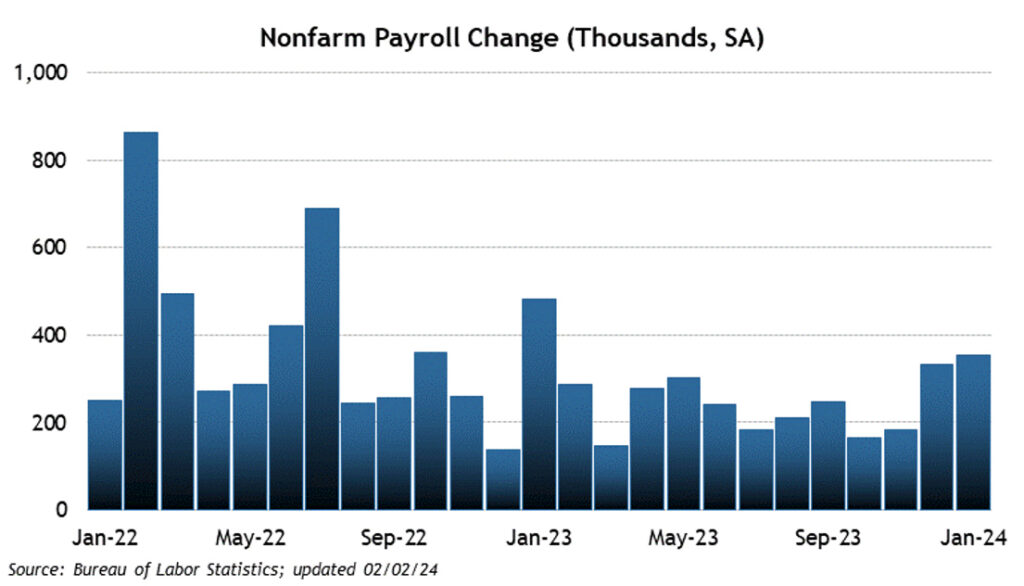

The January Employment Situation report showed an increase of 353K non-farm payrolls more than double what had been expected. The Unemployment rate stayed steady at 3.7%, which was less than the estimated 3.8%. Average Hourly earnings increased by 0.6% in January, double the consensus estimate of 0.3%. The Average work week declined to 34.1 hours from 34.4. The robust payrolls report on Friday sent US Treasuries lower across the curve and induced a sell-off in the interest sensitive sectors of the equity market. Interestingly, the stronger payrolls number came after a weaker than expected ADP number and a slight up tick in the job openings data. The high frequency data of Initial Jobless Claims and Continuing Claims weakened last week as headlines showed substantial layoffs in corporate America. The increase in wages on the Payroll report were tempered by the first look at Q4 Productivity, Unit Labor Costs and the Employment cost Index. Productivity came in at 3.2% vs. 1.8% while Unit Labor Cost and the ECI came in less than the consensus estimates. US manufacturing data was also better than expected coming in at 49.1 versus the estimate of 48. The final reading of the January University of Michigan Consumer Sentiment index came in at 79, the best level since July of 2021.

Corporate earnings for the 4th quarter continued to come in and surprise. Meta was a standout this week, increasing over 20% after their earnings announcement and set a record for market cap gains in a single day. Cost cutting measures propelled the company to better than expected results and the announcement of the company’s first dividend along with a 50 billion dollar stock repurchase o der solidified the idea that the company is in a great position. Meta also announced more cap-ex spending on its AI initiatives. Microsoft, Google, Apple, and AMD also posted better than expected results but there was a sense that some of their recent price appreciation was already incorporated in their prices. A Bloomberg headline described the differential in price action post earnings in the Magnificent 7 as “splintered” and I must agree. Tesla and Apple have been laggards while the other 5 names continue to pull the indices higher.

The S&P 500 and Dow forged another set of record highs. The S&P 500 gained 1.4% as did the Dow. The NASDAQ advanced by 1.1% while the rate sensitive Russell 2000 lagged with a loss of 0.9%. Oil prices cratered losing 7.3% or $5.77 to close at $72.07 a barrel. Gold prices rose by 1.8% or $36.60 to $2053.60 an Oz. Copper prices fell by 0.03 to $3.82 per Lb. The US dollar Index climbed 0.4% to close at 103.54. US Treasuries had a wild ride over the week. Early trade saw yields decrease substantially only to be met with a strong sell off after the robust Employment Situation Report. Despite the strong sell off on Friday the 2-year yield closed down by two basis points to 4.38% as the 10-year saw its yield decline by thirteen basis points to close the week at 4.03%

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involve risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted

{kind=link}

{kind=link}

Weekly Market Commentary – 12/30/24

Read more